Stabilization rather than acceleration. That was the name of the game for the promotional products industry as 2025 came to a close.

PPAI Research’s most recent bi-monthly survey has confirmed that the industry grew by 1.9% in November and December compared to the same two-month period in 2024. This is an uptick from the 1.45% it was up in September and October.

- Still, that growth is below the rate of inflation, which currently stands at 2.7%, and tariff complications continue to create hurdles for firms on all sides of the supply chain.

- The latest revenue data isn’t cultivated from the same methodology as the annual U.S. Distributor Sales Volume Estimate, which polls U.S. distributors of all sizes.

- Rather, the current assessment stems from the aggregated results of PPAI 100 distributors and suppliers responding to a flash survey.

According to Alok Bhat, market economist and PPAI’s research and public affairs lead, the data reinforces a channel level divide where demand remains steady, but cost pressures continue to shape performance differently across suppliers and distributors.

“The industry isn’t accelerating, but it’s not pulling back either,” Bhat says. “Stability right now is being earned through pricing discipline and execution.”

Supplier Findings

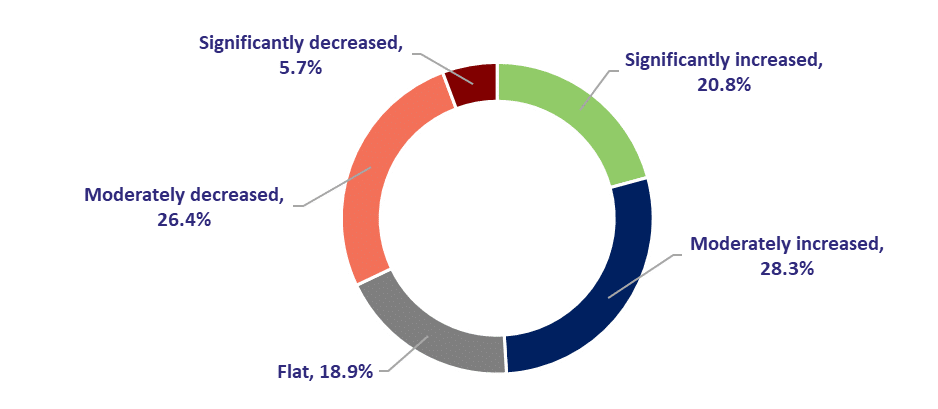

Nearly half (49%) of PPAI 100 suppliers reported year-over-year revenue growth in November and December.

- Nearly one-third (32%) reported revenue declines while 19% reported flat revenue.

- Importantly, declines were largely moderate (26%) rather than significant (6%), pointing to cautious purchasing and selective demand.

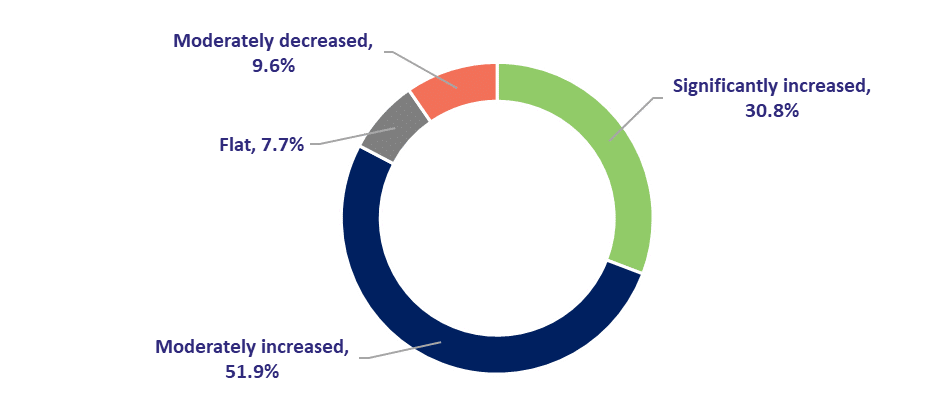

In addition to freight volatility and tariff-related uncertainty continuing to pressure margins, 64% of suppliers also faced higher procurement costs during the period.

- Nearly one-third (31%) reported that procurement costs remained flat, showing limited cost relief across the supply chain.

Despite stable sales conditions, profit margins remained under pressure for many PPAI 100 suppliers.

- 46% reported margin declines due to inflation, with 44% experiencing slight decreases and 2% reporting significant declines, while 40% reported no material impact.

Only 14% saw margin improvements, reinforcing that rising costs have not been fully offset by pricing, even as sales showed signs of stabilization.

“Promo is holding its ground,” Bhat says. “The work is there, but margins and costs are deciding who actually benefits.”

Alok Bhat

Market Economist, Research & Public Affairs Lead, PPAI

Distributor Findings

PPAI 100 distributors demonstrated relatively stronger momentum, supported by pricing discipline, program-based revenue and greater flexibility in managing client budgets.

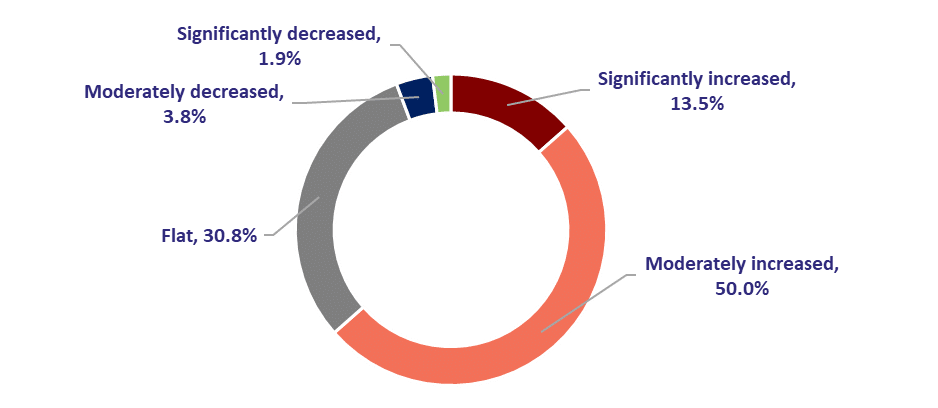

- Nearly 83% of PPAI 100 distributors reported year-over-year revenue growth in November and December.

- Approximately 8% reported flat revenue, while about 10% experienced declines, reflecting generally steady but uneven demand.

“Orders are moving and programs are active, but cost pressure hasn’t gone away,” Bhat says. “This is a year where how you run the business matters as much as demand.”

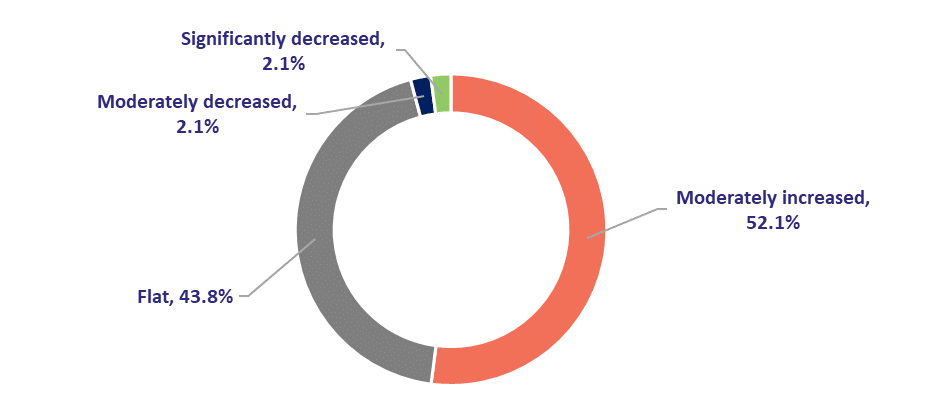

Sourcing challenges remained for distributors as well, with more than half (52%) reporting higher procurement costs and 44% saying procurement costs were flat or predictable.

Profit margins for PPAI 100 distributors remained largely stable, with inflation continuing to create modest pressure.

Nearly 59% reported no material impact on margins, while 24% experienced slight margin declines, indicating that inflation effects were present but generally manageable within current operating models.

- At the same time, 17% reported margin improvements, mostly modest.

“Across both groups, cost relief remained limited, reinforcing that late-year performance was driven more by execution and pricing management than by a broad-based rebound in demand,” Bhat says.