The branded merchandise industry enters mid-year 2026 with strong consumer relevance, positive but measured growth and a rapidly changing operating environment.

Demand isn’t the core problem. Consumers continue to value useful, well-designed merchandise and end buyers are using branded products across campaigns, events, employee engagement, recognition and customer experience.

What is changing is how value is created, delivered and retained.

Tariffs and cost volatility are reshaping margins. Different orders are moving through different sourcing and service models. Strategic accounts are receiving deeper attention, while routine business moves toward digital channels. AI is beginning to separate firms that remove friction from those carrying manual cost through every transaction. At the same time, branded merchandise is being used more strategically than it’s being funded or measured.

These six shifts define the industry’s mid-year outlook.

Trend 1: Growth Shifts From Volume To Value Capture

The industry is still growing, but the basis of growth is changing. Revenue alone no longer tells leaders whether a business is truly expanding because pricing and product mix are supporting the top line even when unit demand is uneven. In March and April, PPAI 100 suppliers grew approximately 1.1%, while distributors grew about 2%. Supplier unit performance was weaker and more uneven than revenue, suggesting that recent gains aren’t coming from broad demand acceleration alone.

The clearest signal is at the higher-value end of the market. Retail-branded merchandise reached approximately $6 billion in 2025 and grew 13.4%, far outpacing the broader distributor market. Consumers reinforce the same message: 83% say receiving a promotional product makes them feel appreciated, 90% feel more positive about the brand, 94% are likely to keep selected products for at least six months and 74% still use the last few products they received.

The implication isn’t that every order should become more expensive. A premium product with little relevance can still fail. The real shift is toward greater value in every order through usefulness, durability, design, personalization, execution and clear campaign purpose.

A distributor, for example, can create more defensible value by turning a basic employee kit into a coordinated onboarding program with product curation, personalization, fulfillment and measurement. The unit count may be similar, but the strategic value and margin opportunity are materially higher.

Accenture Life Trends also highlights growing consumer hesitation around online content and the importance of trust. In that environment, useful physical merchandise can give a campaign tangible presence and extend its life beyond another fleeting digital impression.

It’s not about more stuff. It’s about better-value merch that feels useful, premium, relevant and worth keeping.

Trend 2: In The Wake Of Tariffs, Margin Pressure Is Structural

Tariffs may be the most visible source of pressure, but they’re part of a broader reset in the economics of branded merchandise. Procurement costs, freight, compliance requirements and tighter client budgets are becoming the industry’s operating baseline.

Among PPAI 100 suppliers, 60% report higher landed product costs, 60% cite pricing uncertainty and 51% report reduced gross margins. Only about 10% are passing through most of the additional tariff, freight and input costs, while more than a third continue to absorb most or nearly all of the impact.

Distributors face less direct margin damage, but the pressure appears elsewhere. More than half (56%) report higher supplier costs, 44% cite pricing uncertainty, and 42% say customer decisions are being delayed. Buyers are asking more questions, seeking alternatives, reducing orders or taking longer to commit.

Don’t Miss A Thing: SUBSCRIBE To PPAI Newslink

The sourcing response is significant but selective. More than half of suppliers are diversifying countries of origin, 41% are increasing inventory on selected products and 29% are renegotiating vendor terms. Domestic and nearshore sourcing remain constrained: 74% cite higher cost, 42% limited availability and 42% customer unwillingness to pay a premium.

Kearney’s 2026 Reshoring Index reflects the same pattern. U.S. manufactured-goods imports reached a four-year high despite major domestic investment and tariff activity. Supply chains are changing, but production is often shifting from one overseas market to another rather than simply returning to the United States.

The advantage is no longer one lowest-cost source. It is the ability to offer reliable alternatives and explain the tradeoffs clearly. More than 70% of PPAI 100 suppliers and distributors also identify tariff predictability and trade stability as a leading advocacy need.

Tariffs, procurement costs, freight, compliance requirements and tighter client budgets are no longer temporary disruptions. They now define the industry’s operating norm.

Trend 3: Channel Bifurcation By Use Case

Branded merchandise no longer moves through one universal channel path. Different orders now require different operating models.

A small order may move through a distributor website, client portal or automated reorder system. A strategic employee engagement program may require distributor-led product curation, compliance, fulfillment and reporting. Premium gifting may rely more heavily on retail brands, packaging and presentation, while compliance-heavy programs are more likely to remain within trusted supplier and distributor relationships.

Large, predictable orders follow another path. A Fortune 500 company planning a major event, sports activation or national campaign may know its volume and timing months in advance. At that scale, the buyer may source directly from a manufacturer or overseas factory, bypassing parts of the traditional channel.

Alok Bhat

PPAI Research & Public Affairs Lead

That isn’t only a threat. It’s a growth opportunity. Suppliers and distributors that combine direct-factory economics with quality control, compliance, decoration, logistics, fulfillment and one point of accountability can compete for work that might otherwise leave the channel.

Distributors generated about $4.4 billion in 2025 sales through non-industry suppliers, equal to 16.3% of industry sales. Online sales reached $7.1 billion, or 26.3% of distributor revenue. At the same time, 53% of distributors say they’re relying more heavily on preferred or trusted suppliers as volatility continues.

The route to market will increasingly be determined by each order’s scale, purpose, complexity and risk.

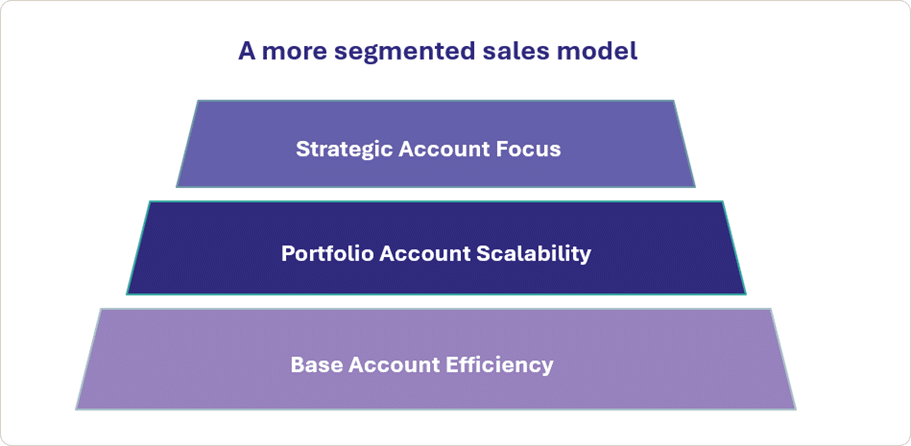

Trend 4: Strategic Attention And Scalable Service

When the external market changes, the internal operating model must change with it.

As margin pressure becomes structural and the channel splits by use case, one-size-fits-all sales and service become harder to sustain. Firms must decide where to apply high-touch resources and where to scale service efficiently.

Strategic accounts require dedicated managers, deeper planning, program management, sourcing expertise and fulfillment coordination. Portfolio accounts can be served through shared teams, standardized playbooks and consistent service levels. Routine demand can increasingly move through portals, automation and digital-first channels designed for speed and a lower cost to serve.

This model reflects where distributors create value. Nearly 60% of PPAI 100 distributors report that 90% to 100% of their value creation occurs in the United States through sales, account management, program coordination, fulfillment, compliance and client service.

AI and automation will make segmentation more practical by supporting quoting, product recommendations, CRM prioritization, reorder prompts and routine communication. Human attention can remain focused on relationships, judgment and complex problem-solving.

The next growth model will depend on human attention where complexity and value are highest and on scalable service where speed and efficiency matter most.

Trend 5: Technology Is Becoming The Margin Engine

AI is moving from experimentation to operating infrastructure. Nearly 70% of responding PPAI 100 firms report that they have integrated AI or are actively testing it, while another 20% plan to adopt it within the next 12 months.

The shift is also visible in how distributors go to market. Online sales reached $7.1 billion in 2025 and grew 4.5%, outpacing overall industry growth. More than 4 in 10 distributors said digital marketing and e-commerce increased sales, while 35% reported integrating technologies such as AI, AR or VR into marketing or selling.

The immediate opportunities are practical: faster quoting, product discovery, artwork support, CRM prioritization, sourcing comparisons, reorder prompts, customer service and compliance documentation. AI can also evaluate landed costs, recommend alternatives and improve responses when tariffs, inventory or lead times change.

The Expert Panel: How Is Technology Reshaping Your Business?

Many margin challenges are operational. Time is lost searching for products, rebuilding quotes, correcting artwork and handling routine requests manually. Across thousands of orders, those inefficiencies become a significant cost to serve.

The next phase will go beyond isolated tools. Agentic AI could connect multiple order steps, while industry-specific models may improve accuracy in product data, decoration, sourcing and compliance. Firms with clean data, consistent processes and clear governance will benefit most.

AI won’t replace relationship selling – it’ll expose slow workflows, weak data and manual operating models.

Treat AI as an operating model decision, not a pilot program.

Trend 6: Used Strategically, But Still Budgeted Tactically

Branded merchandise is increasingly used across campaigns, events, employee engagement and customer experience, but it’s still not consistently funded or measured like a primary marketing medium.

Nearly half (47%) of distributors say end buyers use branded merchandise as a core marketing channel, and 25% say it’s important for specific campaigns. Yet only 21% say it holds a core place in marketing budgets, while 50% cite difficulty proving ROI.

The consumer evidence is strong: 90% say promotional products make them feel more positive about a brand, 80% have looked up or purchased from a brand after receiving one, 51% prefer receiving a promotional product over ads, emails, texts or sales calls, and 84% say merchandise improves their impression when included in an event or campaign.

The strongest programs will connect physical and digital experiences. A product can drive someone to a landing page, extend an event experience, unlock content through QR or NFC technology or reinforce a campaign long after the first impression.

The challenge is measurement. The industry must help buyers connect merchandise to recall, engagement, retention, participation, loyalty and customer action.

Branded merchandise is increasingly used like a primary marketing channel, but still budgeted like a secondary one. Closing that gap is one of the industry’s biggest growth opportunities.

The Outlook

The next phase of growth will not come from selling more units alone. It will come from firms that create more value in every order, protect margin through volatility, match the channel model to the use case, segment accounts deliberately, use technology to remove friction and prove branded merchandise as measurable marketing impact.

The industry still has consumer permission and end-buyer relevance. The opportunity now is to turn that relevance into more defensible, profitable and measurable growth.

- For more details, log on to PPAI Premium Research.

A market economist, Bhat is research and public affairs lead at PPAI.